The Flawed Social Security Advice Thats Being Spread by Finfluencers

November 20, 2025

by K. Jeremy Ko

Have you seen the argument to claim social security benefits early (i.e., at age 62) that has been making the rounds? The argument is that you should claim your social security retirement benefits early because you can reinvest benefits in the stock market at high rates of return. You can find it across social media in YouTube videos and even in respected publications like the Wall Street Journal.

Don’t get me wrong. There are some legitimately good reasons for claiming social security at age 62 and not postponing until age 70. For example, many people need the money upfront and can’t afford to postpone their benefits.

It’s just that this particular argument is flawed. A variation of this argument is to claim social security early because you’d otherwise need to withdraw money from your investment portfolio – which can earn high rates of return. Let’s put the argument to rest. Or at a minimum, let’s place some heavy caveats on it. It runs contrary to basic principles of economics I discuss below.

On its surface, the argument sounds entirely reasonable – which is why it’s run rampant. We can even construct a numerical example which supposedly demonstrates its validity.

Let’s take a person with a benefit of $2000 per month at their full-retirement age (age 67 for anyone born in 1960 or later). That person would earn $1400 per month in real terms (i.e., in terms of the amount they can buy) if they claimed at age 62. They would earn quite a bit more – $2480 per month – if they waited until age 70 to claim.

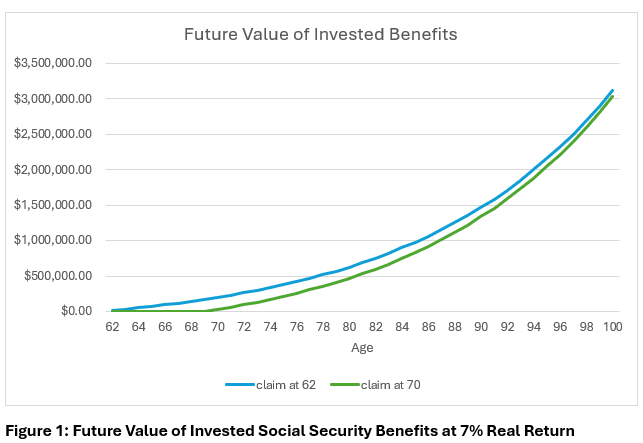

Now let’s compare claiming at age 62 vs. 70 if you were to invest your monthly benefits in the stock market at a real return of 7% per year – which is roughly equal to its historical average return. The graph in figure 1 above shows that you’d have more money through age 100 from claiming at age 62. Therefore, it makes sense to claim at age 62 and invest in the stock market, right? Wrong!

So what are the problems with the argument?

Problem 1: The argument doesn’t account for RISK.

The fact is that the stock market may not return 7% per year after you claim your benefits. Stock market returns are inherently risky. For example, the average real return on the US stock market was -3% per year from 2000 until 2009.

In contrast, social security benefits have historically been predictable and stable in real terms (i.e., they adjust with the cost of living as they are indexed to inflation). Let’s put aside for a moment forthcoming issues with the solvency of the social security system – which we will discuss in a future blog.

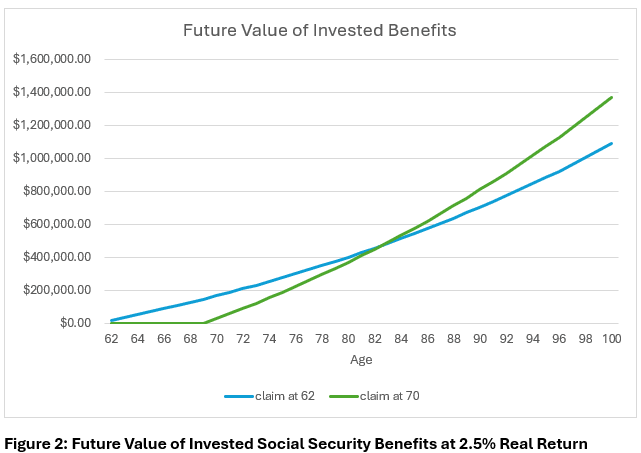

Therefore, because of risky returns, you may not get $200K by age 70 from claiming at age 62 as shown in the graph above. You may get something far less than that if a bear market ensues. This means you shouldn’t inflate your age 62 benefits by the average return on the stock market when comparing them to age 70 benefits. Instead, you should inflate them by a low-risk, stable return to match the risk of your future benefits. A return of 2-3% (based on historical real treasury rates) would be more appropriate.

Figure 2 above shows how much you would have from investing your social security benefits at a real rate of return of 2.5%. In this case, you would have $167K at age 70 if you were to claim at age 62. You would have $543K at age 85 (the current median lifespan for US adults alive at age 62). In contrast, you would have $577K at age 85 if you were to claim at age 70.

Problem 2: The argument assumes that people should BORROW to fund stock market investment.

Wait a second. Why is claiming at age 62 akin to borrowing money? After all, I’m not signing a loan contract when I claim early. There’s no credit check, no co-signer, no prospect of default, etc.

The fact is that claiming at age 62 is ECONOMICALLY equivalent to borrowing money from your future benefits – even though it doesn’t legally constitute borrowing. Think about what happens if you were to take a loan which pays you from age 62 to 70 which you then need to pay back from age 70 until the end of your life. This kind of contract is like a college loan – except that it would be for old people (like myself).

You would receive payments from age 62 to 70. You would then pay back your loan in monthly installments starting at age 70. If you were to claim social security at age 70, you would receive your delayed social security benefits minus the loan repayments.

And this is EXACTLY what happens when you claim early at age 62! You get benefits from age 62 to 70 and continue to get benefits from age 70 on – which are LESS than you’d otherwise get from claiming at age 70. You’re effectively paying back your loan for benefits from age 62 to 70 in the form of lower benefits from age 70 on.

There are some people who could conceivably LIKE taking a loan to fund stock investment. But these people are few and far between. In fact, people with high work income before their full-retirement age (e.g., age 67) do not have access to early social security benefits because of work penalties (see here). I’m not aware of any of these people who have taken a loan prior to age 67 because they want additional money to invest in the stock market starting at age 62.

In Conclusion

Again, I’m not trying to argue that no one should claim their benefits at age 62. Good reasons for claiming early include financial need and short expected lifespan. However, don’t let a finfluencer or your advisor talk you into claiming early so you can invest in the stock market without thinking through the hidden assumptions that I discuss here.

Your Retirement Partner

Discover strategies to secure your financial future.

Contact us today through our easy form for personalized advice on maximizing retirement income and planning for long-term care.